Students / Educators / Employers & Professionals

Please sign up below for more information about

our programs for verified trading credentials

The Learning Center is a reference area for many common questions and concepts that you may encounter while competing in competitions and constructing portfolios.

General Competition OverviewThe general competition starts as soon as a student logs the first trade. Students should try their best to construct a diversified book of positions that will out-perform the Russell3000 index and reduce volatility. ALPHASEAL normalizes performance from competitors who start on different dates by using average daily statistics when applicable for ranking factors and by using Net Benchmark Outperformance rather than Portfolio Net Return. It could be argued that the longer the track record, the lower the Volatility metric is likely to be. Volatility of Daily PNL is the only metric where lower is better, so starting sooner can theoretically improve a student’s standing in the General rankings.

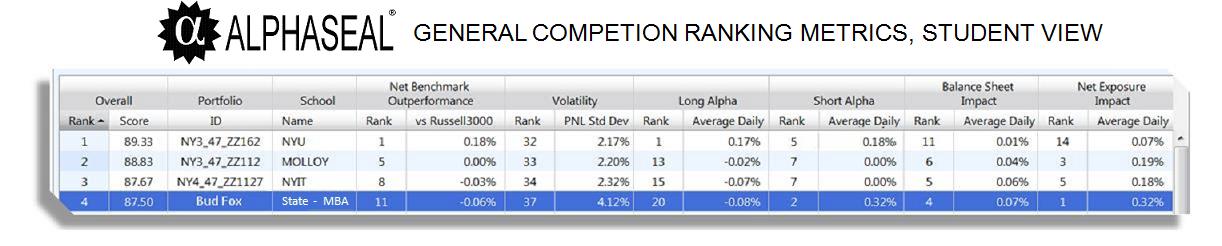

General Competition Rankings Methodology

Each of the six General Competition Ranking Metrics are added together and the lowest combined score wins. Overall ranking is presented as the arithmetic average of all six rankings subtracted from 100. In the example below, the Overall rankings are calculated as follows:

1) +14+11+5+1+32+1 = 64; 64/6 = 10.67; 100 – 10.67 = 89.33

2) +5+33+13+7+6+3 = 67; 67/6 = 11.17; 100 – 11.17 = 88.83

3) +8+34+15+7+5+5 = 74; 74/6 = 12.33; 100 – 12.33 = 87.67

4) +11+37+20+2+4+1 = 75; 75/6 = 12.50; 100 – 12.50 = 87.50.

Net Benchmark Outperformance = PNL (%) – Benchmark Performance

Benchmark Performance (Units: %)

For the Fall 2012 competition, the Benchmark is the Russell3000, as measured by the published closing prices for the ticker ^RUA.

For any given period, Benchmark Performance is defined as:

[(Benchmark Closing Price) / (Benchmark Opening Price)] - 1

Benchmark Opening Price = ^RUA Opening Price from the first day of the Competitor’s track record.

Benchmark Closing Price = ^RUA Closing Price, most recent available.

Volatility is defined as the standard deviation of daily PNL (%).

Balance Sheet Impact

Balance sheet impact measures the effect of leverage on a competitor’s portfolio.

Balance sheet impact = PNL – [(PNL) / (Gross Exposure)]

Net exposure impact measures the amount of PNL explained by the competitor’s daily Net Exposure. Knowing when to lever into Beta and when to protect against downside moves in Beta is considered a

part of the skill set required in professional asset management. Net Exposure Impact tests for that. It is presented in the top line on the “Period Summary” page on ALPHASEAL® as an average daily statistic.

We use average daily to normalize for students that start on different calendar days. If you believe you are a skilled trader, then more days should be better for your track record.

For calculating daily statistics:

Net Exposure Impact (%) = Net Exposure (%) * PNL (%) = Net Exposure Impact (%)

For calculating periodic statistics:

Portfolio Average Daily Net Exposure Impact (%) = [Sum of (Net Exposure Impact) for all trading days the Portfolio participated in the competition]/[# of trading days Portfolio participated in the competition]

Opening Equity for a given period is defined as the previous day’s Closing Equity.

Closing Equity (Units: $’s)

Defined as the liquidation value of a portfolio assuming no transaction costs to liquidate.

This is a methodology for measuring the net worth of an investor’s assets under management.

There are many ways to measure this, and no one definition has definitive authority. Since we are dealing with simulations of publicly traded securities whose day-end prices are generally available, we have used that in our current approach. Change in Equity represents inflows and redemptions of capital into a portfolio. For our purposes, this has an impact in Period 1 only.

Period 1 Total Equity = 0 + Change in Equity Period 1 (Starting capital of $100,000.00)

Period 2 Total Equity = Period 1 Total Equity + Period 1 PNL + Change in Equity Period 2

Period 3 Total Equity = Period 2 Total Equity + Period 2 PNL + Change in Equity Period 3

Period n Total Equity = Period (n-1) Total Equity + Period (n-1) PNL + Change in Equity Period n

Defined as the Net Asset Valuation for the end of the period being measured.

This is a methodology for measuring the growth in value of an investor’s capital on a relative basis.

The convention is to start at 1.00 or 100%. There are reasons to use other first period values, but for now we’ll assume NAV in period 1 = 1. Everything below is at the “portfolio” level. So the complete nomenclature would be “Period 1 net asset value for this portfolio is 100%.”

Period 1 NAV = 1

Period 2 NAV = Period 1 NAV * (2 + Period 2 PNL)

Period 3 NAV = Period 2 NAV * (1 + Period 3 PNL)

Period n NAV = Period (n–1) NAV * (1 + Period n PNL)

We sometimes use “PNL” as shorthand for “Portfolio Net Return.”

This is a methodology for measuring periodic performance of a portfolio on a relative basis and is often expressed as a percent.

Period 1 PNL (%) = (Period 1 PNL) / (Period 1 Opening Equity)

Period n PNL (%) = (Period n PNL) / (Period n Opening Equity)

Profit and loss is the measurement of gains and losses that an investor’s portfolio experiences in a given period. In addition to trading gains and losses, an investor will experience transaction costs such as interest fees/payments and costs of associated with maintaining and transacting in their brokerage account. Dividends, coupon payments and other investment proceeds or outflows may be recorded on a periodic basis as well. PNL does not include a measurement for new capital that flows into a particular portfolio or that is redeemed and flows out from a portfolio.

Period 1 PNL ($’s) = Sum of (Period 1 Trading gains/losses + Period 1 interest payments/fees + Period 1 brokerage fees + Other investment inflow/outflows).

Period n PNL ($’s) = Sum of (Period n Trading gains/losses + Period n interest payments/fees + Period n brokerage fees + Period n Other investment inflow/outflows).

The take-away lesson of the Henry Blodget settlement is: an analyst is required to be consistent in her/his private opinions and public opinions.

The United States securities regulations require professional financial analysts to have “a reasonable basis, present a fair picture of the investment risks and benefits, and not make exaggerated or unwarranted claims” in their published research reports. According to the Henry Blodget settlement, the regulators charged that Mr. Blodget published “research in which he expressed views that were inconsistent with privately expressed negative views.”

http://www.sec.gov/news/press/2003-56.htm

It was also notable because Eliot Spitzer released emails that included contradictory opinions without pressing any formal charges. The take-away lesson to the industry was: you can be held accountable for everything you write in an email.

All interest calculations work from a base rate that is set to equal Broker Call. Also known as the Call loan rate, it is the interest rate relative to which margin loans are quoted by broker dealers. The rate is published daily in financial publications and is currently 2%. All interest is calculated from this rate on the platform as follows:

Cost of Margin = Base Rate + 2% = 4%

Cash Interest = Base Rate – 1.75% = 0.25%

This interest is charged on all Margin balances and paid on all cash balances on a weekly basis. Your ability to utilize margin is governed by Reg-T, the regulatory limits for retail investors. This will impact your buying power and any margin call decisions that may impact you. At the inception of the competition your buying power will be 2x your cash balance. As you move forward and have securities in your account, your buying power will be 2x the combined equity and cash balance less a haircut for securities that is driven by the liquidity in those issues. Margin call decisions, primarily forced liquidation, will be imposed should the combined equity and cash value of your account drop below 30% of the total value of securities held.